China Archives - Leeham News and Analysis

China's relationship with Western commercial aircraft manufacturers remains one of the most consequential and politically entangled dynamics in global aviation, shaped by trade policy, national pride, and long institutional memory. Airbus faces a conspicuous absence of A220 sales in a country where it has otherwise built deep manufacturing and commercial ties, including a 737-class A320neo family final assembly line in Tianjin and an A330 finishing line. Despite the fact that fuselage sections for the A220 have been produced in Shenyang since the aircraft's Bombardier C Series era, not a single A220 has been ordered by a Chinese carrier or lessor. Airbus Canada executives, speaking at a June 2026 media briefing at Mirabel, attributed this directly to political fallout from the 2017-2018 transaction in which Bombardier sold the C Series program to Airbus after Chinese entities had actively participated in a bidding process for the program. As head of single-aisle market development Christian Kley noted, "They have long memories" — a candid acknowledgment that the Chinese government's procurement decisions for state-controlled airlines carry geopolitical weight that extends a decade or more.

The Boeing side of the China equation is no less complicated. Reports from August 2025 indicated Boeing was approaching a potential deal for up to 500 aircraft with Chinese carriers, a transaction that would represent a landmark reopening of a commercial relationship frozen since 2017. That freeze has been the product of cascading policy decisions: Trump-era tariffs in his first term, Biden-era retention of those tariffs plus additional economic sanctions tied to China's alignment with Russia following the 2022 Ukraine invasion, and then a new round of tariffs imposed when Trump returned to office in 2025. Beijing's 2019 grounding of the 737 MAX — which lasted far longer than any other regulator's, ending only after the FAA's November 2021 recertification — deepened the commercial estrangement and created a demand gap that China's homegrown COMAC C919 cannot yet fill at scale. Leeham News analysis has consistently argued that China's domestic air travel growth outpaces C919 production capacity, meaning the country structurally needs Boeing aircraft even as its government uses procurement as a diplomatic lever.

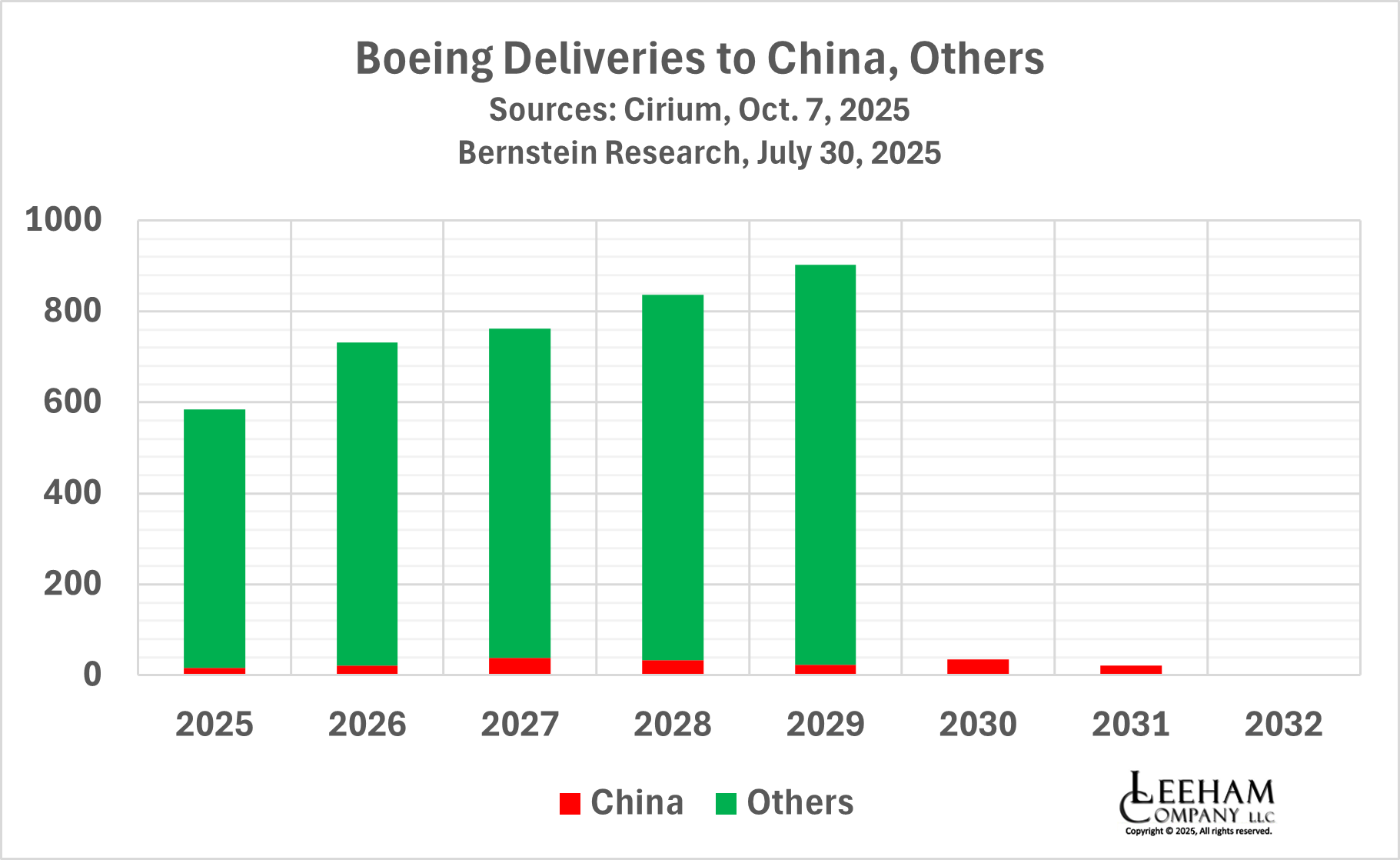

Despite the headline drama around Trump's October 2025 announcement of 100% tariffs and possible blocking of Boeing deliveries to China, the practical near-term impact on Boeing's production and revenue is limited. Data from Cirium placed Boeing deliveries to Chinese airlines and lessors at between three and five percent of total global deliveries through the end of Trump's current term in January 2029. The tariff threats, while symbolically significant, amount to a small fraction of Boeing's delivery pipeline. The more consequential risk lies not in blocked new deliveries but in the potential disruption to spare parts and component supply for China's existing Boeing fleet — a scenario that could eventually ground in-service aircraft if restrictions were sustained. Notably, Airbus aircraft operated by Chinese carriers are not immune; many contain US-sourced parts, components, and engines, meaning a broad export restriction could affect both manufacturers' installed base simultaneously.

For professional pilots and operators, particularly those flying internationally or managing aircraft acquisition and fleet planning in markets adjacent to China, these developments carry direct operational relevance. The prospect of parts supply interruptions affecting Boeing's large in-service Chinese fleet raises AOG risk questions for any operator sharing supply chains with Chinese carriers, particularly for high-demand rotable components and engine parts. Airlines and lessors watching the near-deal Boeing order should also recognize that a resumption of large-scale Chinese Boeing deliveries would reshape the used aircraft and leasing market globally, affecting valuations of 737 MAX and widebody assets. On the Airbus side, a successful A220 entry into China — should political relations thaw sufficiently — would meaningfully expand the program's order base and manufacturing scale, potentially influencing delivery slots and pricing dynamics for current and prospective A220 operators worldwide.

The broader structural trend across all three stories is that Beijing functions as a single procurement authority across its nominally separate state airlines and lessors, which means commercial aviation decisions in China are inseparable from diplomatic posture. Airbus's decade-long success in China — hundreds of orders tied to its physical manufacturing presence — demonstrates that industrial investment is the price of market access. Boeing's exclusion during the same period, despite a large installed base and pending order activity, shows how quickly that access can be revoked. For the global aviation industry, China's market is too large to ignore but too politically sensitive to navigate through commercial logic alone. Manufacturers, lessors, and MRO providers must treat Chinese market access as a variable contingent on government-to-government relations rather than a stable commercial baseline.