Cargo Archives - Leeham News and Analysis

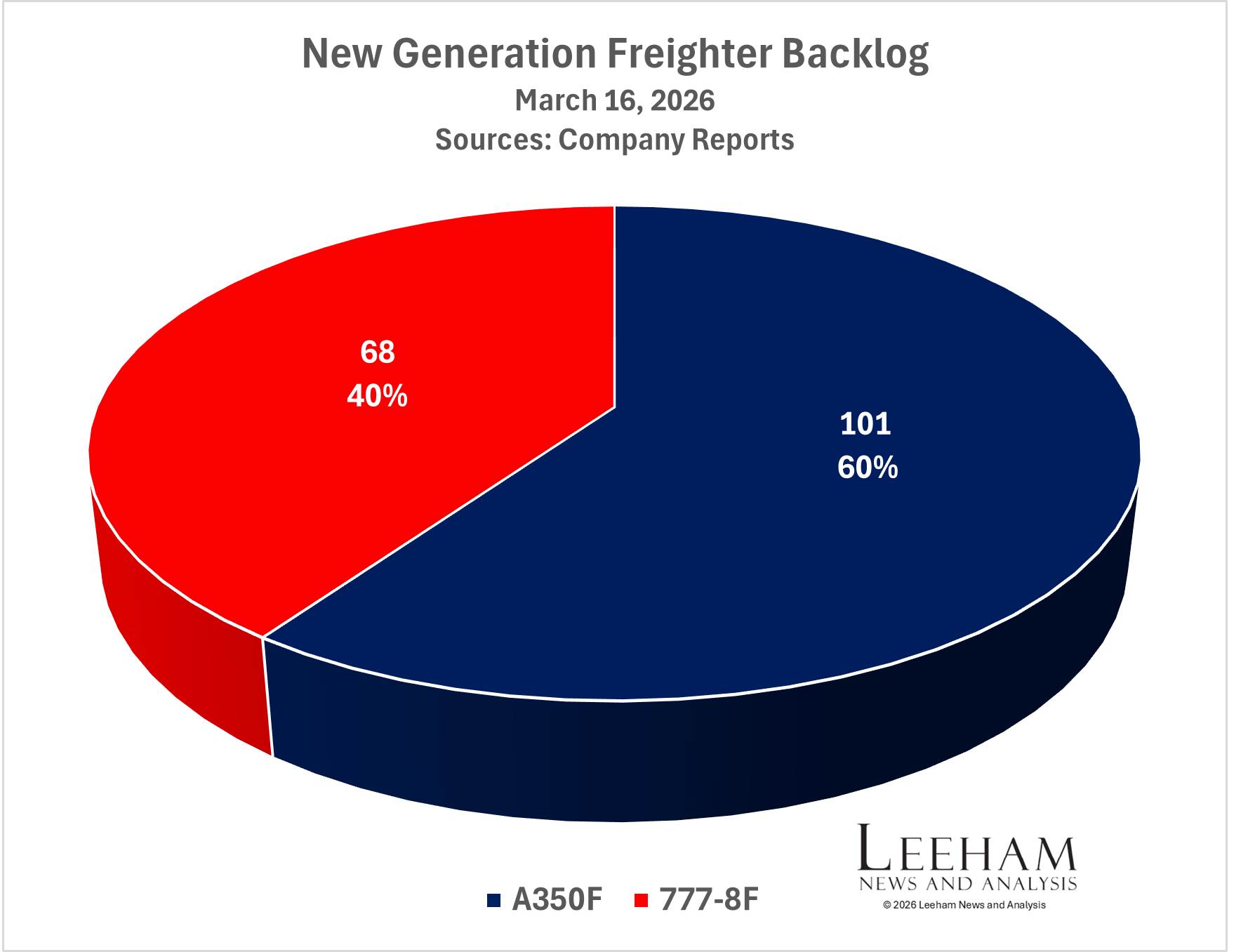

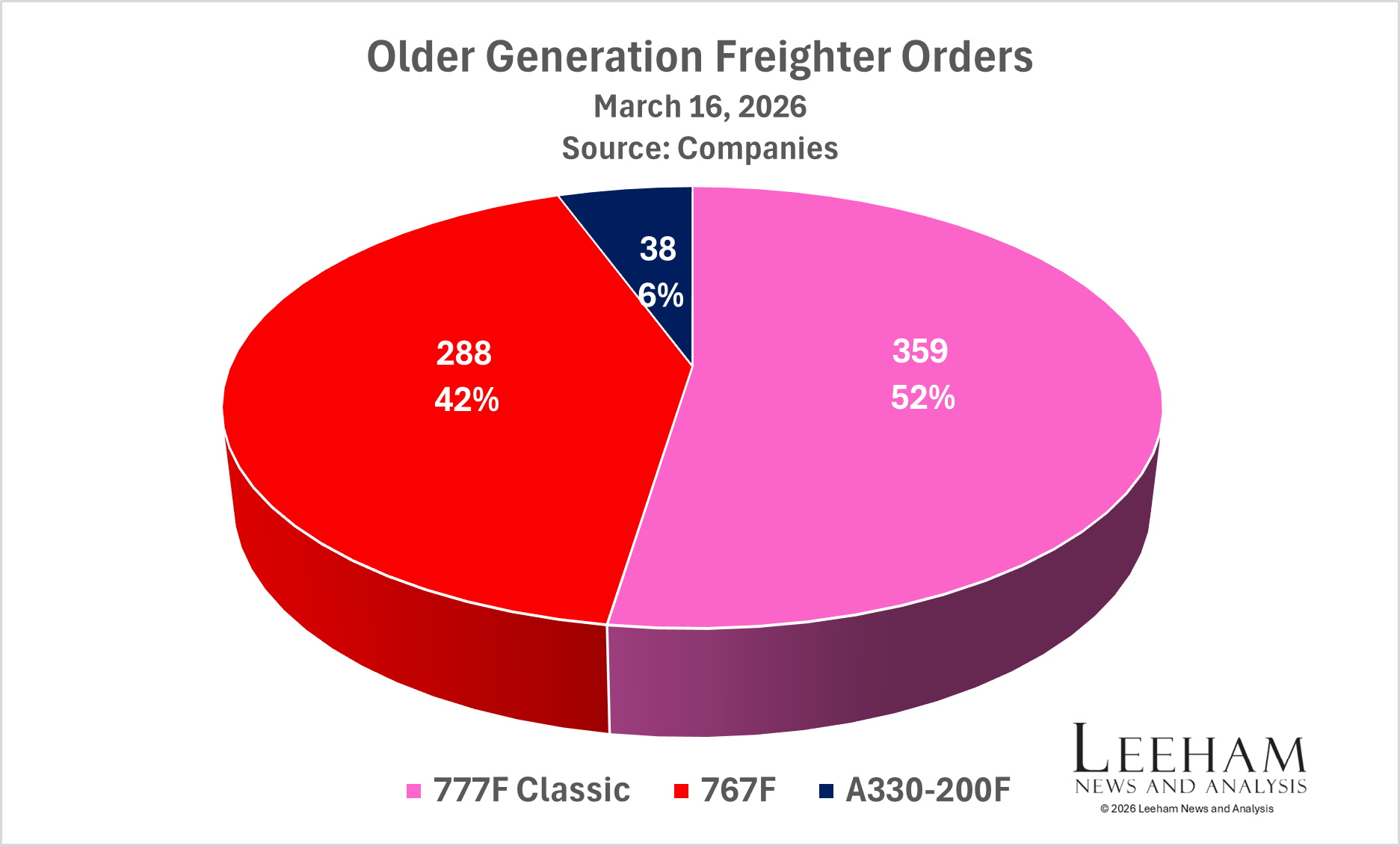

Boeing's decades-long dominance of the commercial freighter market is ending, with Airbus now holding approximately 60% of next-generation freighter orders as of early 2026. The pivot point came in March 2026 when Atlas Air placed an order for 20 A350Fs, pushing Airbus's total A350F order book to 101 aircraft against Boeing's 68 orders for the competing 777-8F. The contrast is stark when viewed against Boeing's legacy freighter record — the 777F Classic accumulated 359 orders over its production life, and the 767-300ERF amassed 288 orders — figures that underscore how thoroughly Boeing once owned the segment. Both legacy programs are slated to conclude production at the end of 2027 due to emissions regulations that neither aircraft's powerplants can meet, and Boeing has sought an FAA exemption to build 35 additional 777F Classics, with a decision requested by May 1, 2026. The old order is closing out even as the new one takes shape around an Airbus-led hierarchy.

The structural causes of Boeing's freighter decline mirror the broader deterioration of the company's competitive standing across all segments. According to Leeham News analysis, the 737 MAX crisis consumed engineering and leadership bandwidth, production suspensions of the 787 disrupted the supply chain and customer confidence simultaneously, and an institutional arrogance — described bluntly as "inbred" — led Boeing to misread key sales campaigns and underestimate Airbus's customer responsiveness. Airbus's approach to the freighter competition is characterized as the tortoise-and-hare dynamic: methodical, customer-listening, and ultimately decisive. The A350F benefits from the same composite-intensive airframe architecture as the passenger A350, offering operators meaningful operating economics improvements over legacy widebody freighters at a time when fuel costs, emissions compliance costs, and cargo yield compression are all pressing issues for cargo carriers.

For cargo operators and the scheduled freighter market — which includes carriers like Atlas Air, FedEx, UPS, and a growing roster of international dedicated freighters — the Airbus shift represents an operational fleet planning inflection point with generational implications. Airlines and cargo operators evaluating widebody freighter acquisitions in the next decade will increasingly be choosing between an A350F ecosystem and a 777-8F program that is still proving itself. The 777-8F's delayed development timeline, rooted in Boeing's broader certification and production challenges, has created a window Airbus has exploited aggressively. For Part 121 operators holding legacy 767-300ERF or 777F assets, the regulatory clock on production and the looming emissions standards are relevant to residual value projections and maintenance planning as the feedstock pool for those platforms eventually stops growing.

The passenger-to-freighter conversion market, covered in adjacent Leeham reporting, adds further complexity to the cargo landscape. IAI's troubled 777-300ER conversion program — with its debut aircraft grounded for months after a single test flight — and Kansas Modification Center's competing forward-door approach both highlight the certification and engineering difficulty of converting large widebodies at scale. Feedstock constraints and regulatory friction are limiting conversion throughput at precisely the moment when cargo demand recovery is creating utilization pressure. These dynamics make new-build freighter orders more attractive to major integrators and dedicated cargo carriers despite higher acquisition costs, which further favors Airbus and Boeing's new-generation programs over the conversion market.

The broader context for professional aviation operators is that the cargo segment is entering a structural reset that will define fleet composition for the 2030s and beyond. The simultaneous wind-down of Boeing's dominant legacy freighter lines, the competitive uncertainty around new-build programs, and the friction in the conversion market represent a trifecta of supply-side disruption in air freight capacity. For flight operations departments, safety officers, and fleet planning teams at cargo carriers and mixed-fleet operators, monitoring both the A350F certification and entry-into-service trajectory and Boeing's ability to deliver the 777-8F on a revised timeline is not merely a financial exercise — it has direct implications for crew training pipelines, maintenance network development, and long-range route network planning across the global cargo system.

Read original article

Read original article