Spirit in the Sky - AskThePilot.com

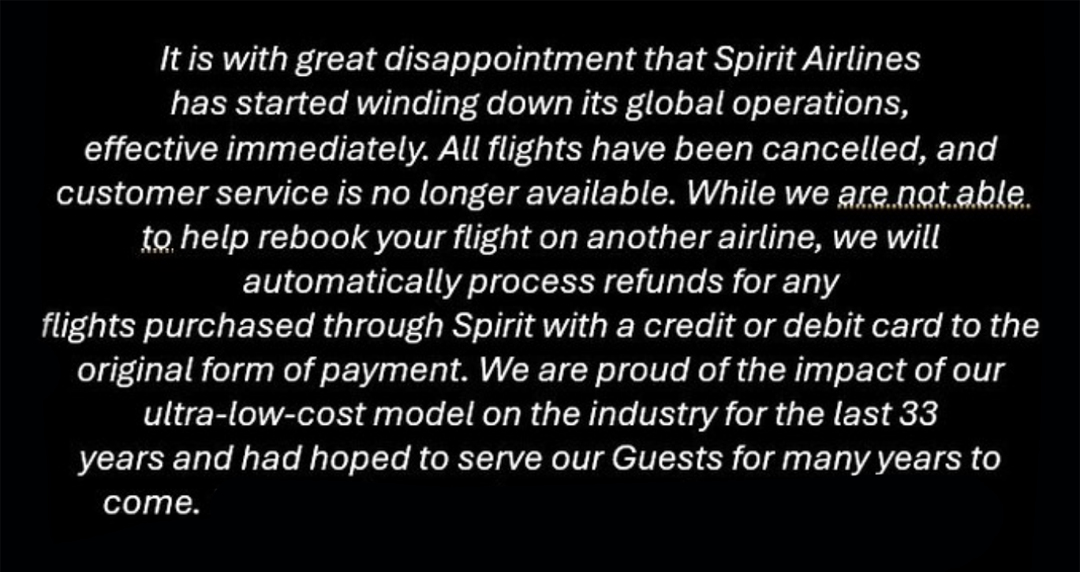

Spirit Airlines ceased operations on May 2, 2026, entering full liquidation and becoming the most significant U.S. airline failure since Pan Am's collapse in December 1991 — a distinction that underscores just how rare outright airline shutdowns have become in the post-merger era. The ultra-low-cost carrier, the nation's seventh-largest by fleet size, operated 130 aircraft and employed approximately 17,000 workers at the time of closure. Unlike the wave of consolidations that absorbed names like TWA, Northwest, Continental, and Piedmont into surviving majors — preserving most jobs while retiring paint schemes — Spirit's shutdown is a complete liquidation, leaving no acquiring entity to absorb its workforce, routes, or aircraft under a unified transition. The carrier's prolonged post-COVID instability, including multiple bankruptcy proceedings, steadily eroded its ability to compete in an ULCC market that demands extreme operational efficiency and razor-thin margins to survive.

For the approximately 2,000 Spirit pilots now unemployed, the practical consequences are defined almost entirely by aviation's seniority system — arguably the most consequential structural feature of airline pilot careers. There is no transfer of tenure in U.S. airline labor. Every former Spirit pilot, regardless of total flight time, command experience, or years with the carrier, must enter any new airline at the bottom of that carrier's seniority list and accept first-year pay rates. For senior Spirit captains with significant turbine PIC time and years of line experience, this calculus is particularly brutal: accepting a position at a major carrier means potentially years of reserve status, unfavorable bidding, junior bases, and compensation that may not reflect their actual experience level for some time. Some will make that transition; others, particularly those closer to retirement age, may calculate that starting over is economically or practically untenable and exit the industry entirely.

The regional carrier segment is absorbing a portion of available hiring, but as the article notes, few Spirit veterans are expected to pursue those opportunities given the pay and quality-of-life tradeoffs involved relative to their prior positions. The major carriers — Delta, United, American — are expected to offer preferential interview slots, a common industry practice during large-scale airline failures, but hiring capacity at that level is finite and will not accommodate the full displaced pilot population. JetBlue and other mid-tier carriers operating in Spirit's former markets may selectively absorb pilots and expand service into vacated city pairs, but the net employment picture across the pilot workforce remains negative in the near term. The broader employee picture — ramp workers, gate agents, dispatchers, maintenance technicians — is bleaker still, as those roles do not carry the same national marketability or licensing portability as ATP certificates.

Spirit's shutdown carries meaningful operational implications for the remaining ULCC and LCC segments of the domestic market. Frontier and Allegiant now absorb the competitive pressure Spirit had concentrated in leisure-heavy, point-to-point, price-sensitive markets. Both carriers will face increased load factor demand and pricing power in routes where Spirit had been a fare-suppressing presence, but they also inherit the reputational positioning — and the social media scrutiny — that Spirit's brand had long absorbed. For corporate and business aviation operators, the disruption is more indirect: Spirit's collapse reduces total domestic seat capacity, tightening commercial options on thinner routes and potentially affecting connectivity for passengers feeding into or out of markets where Spirit had been a dominant or sole low-cost operator. At the charter and Part 135 level, leisure destinations previously served cheaply by Spirit may see incremental demand from travelers who now lack affordable scheduled alternatives.

The shutdown also illustrates the systemic fragility that persists in the ULCC business model when exposed to sustained demand shocks — a lesson with direct relevance for operators and aviation businesses assessing counterparty stability, interline arrangements, and ground service contracts. The collapse of Northeast Express in 1994, described by the article's author from firsthand experience, offers a precise smaller-scale parallel: a code-share partner's withdrawal can trigger immediate and irreversible failure regardless of an airline's operational state at the moment of termination. Spirit's prolonged bankruptcy process provided more warning, but the terminal result — flight operations halting mid-schedule, employees learning of closure in real time — mirrors the same structural reality. For the aviation industry broadly, Spirit's liquidation reinforces that airline business models dependent on sustained volume at minimum yield carry existential risk when revenue environments deteriorate and that recovery from a deep demand disruption like COVID, once structural damage to balance sheets is severe enough, may simply be beyond reach.

Read original article

Read original article